New research from the Consumer Federation of America and the Climate and Community Instituteshows that Maine homeowners with lower credit scores are paying some of the highest insurance penalties in New England. Across the state, families with poor or even average credit face hundreds to over $1,300 more per year in premiums compared to neighbors with excellent credit.

Counties Hit the Hardest

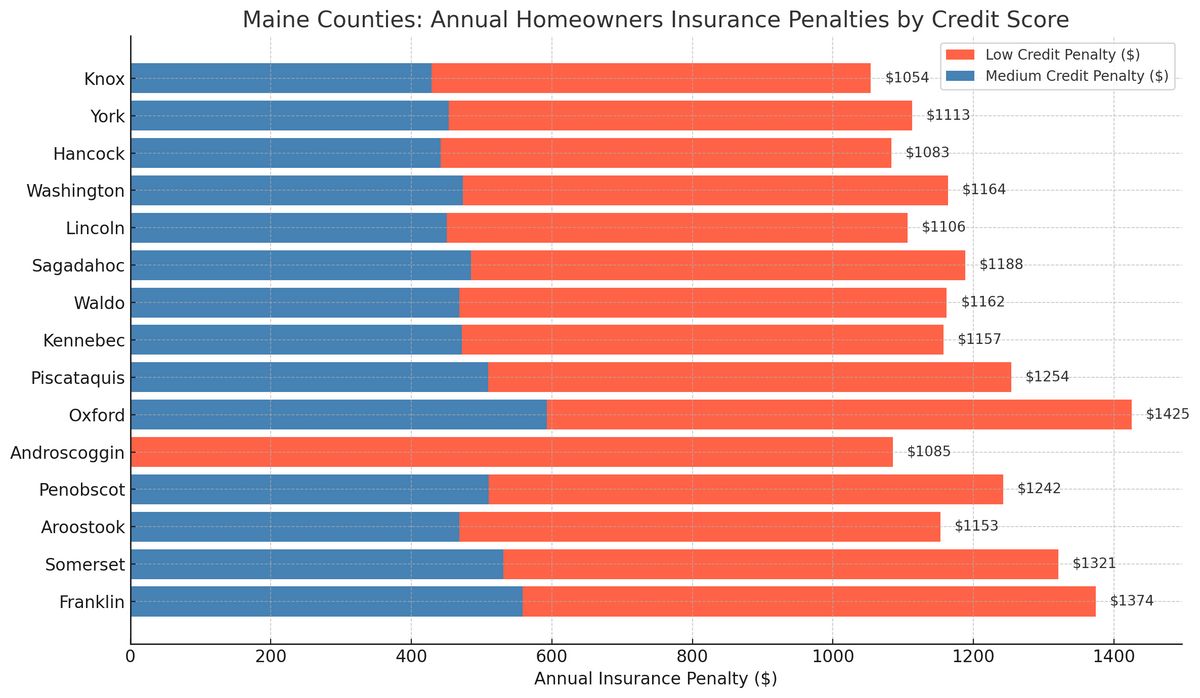

The report, which calculated premiums using data from Quadrant Information Services, found that the penalty for having a low credit score in Maine often exceeds 100%. In other words, insurance costs more than double for otherwise identical homeowners simply based on credit history.

- Franklin County: Homeowners with poor credit pay a 108% penalty—an extra $1,374 per year. Even those with medium credit scores pay 42% more, about $558 extra annually.

- Somerset County: Low-credit homeowners face a 107% penalty (+$1,321), while medium-credit households pay 41% more (+$531).

- Aroostook County: Premiums rise 107% for low-credit households (+$1,153) and 41% for medium credit (+$468).

- Oxford County: The largest dollar penalty—$1,425 per year—hits low-credit homeowners, a 106% increase. Medium credit scores add 41%, or +$593.

- Piscataquis County: Homeowners with low credit scores pay $1,254 more (+106%), and medium-credit households pay +$509 (+41%).

- Kennebec County: The penalty is $1,157 for low credit (+105%) and $472 for medium credit (+41%).

- Waldo County: Low credit adds $1,162 annually (+105%), while medium credit adds $468(+40%).

Other counties across Maine—including Penobscot, Androscoggin, Sagadahoc, Lincoln, Washington, Hancock, York, and Knox—all show similar patterns, with low credit scores adding $1,050 to $1,200 in extra costs per year. Even medium credit scores result in premiums 37% to 41% higher than top-tier borrowers.

Credit Matters More than Risk

The report stresses that in many cases, credit history has a bigger impact on insurance costs than disaster exposure. A homeowner in Maine with poor credit living in a low-risk area can pay more than a neighbor with excellent credit in a higher-risk zone.

What It Means for Maine Families

For households in Maine—especially in rural counties like Franklin, Somerset, and Oxford—the additional burden of credit-based pricing can make homeownership far less affordable.

Consumer advocates argue the practice is unfair, penalizing families who maintain safe homes but lack pristine credit histories. With insurance premiums already climbing due to inflation and climate concerns, the extra cost tied to credit scores can strain budgets further.

Takeaways for Homeowners and Newcomers

If you’re buying in Maine:

- Check your credit before shopping for insurance.

- Compare multiple quotes—companies weigh credit differently.

- Ask about discounts for safety upgrades, newer construction, or bundling with auto insurance.

- Factor insurance into your budget, especially in counties with the highest penalties.

For newcomers relocating to Maine, the message is clear: credit scores matter just as much as location when it comes to protecting your home.